Futures Market: Overnight, LME copper opened at $9,604.5/mt. After fluctuating considerably to reach an intraday low, it surged straight up to a high of $9,636.5/mt, then fluctuated downward. Near the close, it hit a low of $9,578/mt before finally closing at $9,615/mt, marking a 1.24% increase. Trading volume reached 15,000 lots, and open interest reached 286,000 lots. Overnight, SHFE copper was closed for the holiday.

[SMM Copper Morning Meeting Summary] News: (1) Harmony Gold, South Africa's largest gold producer, agreed to acquire MAC Copper for $1.03 billion, which will accelerate the company's strategic shift towards copper through a key asset in Australia.

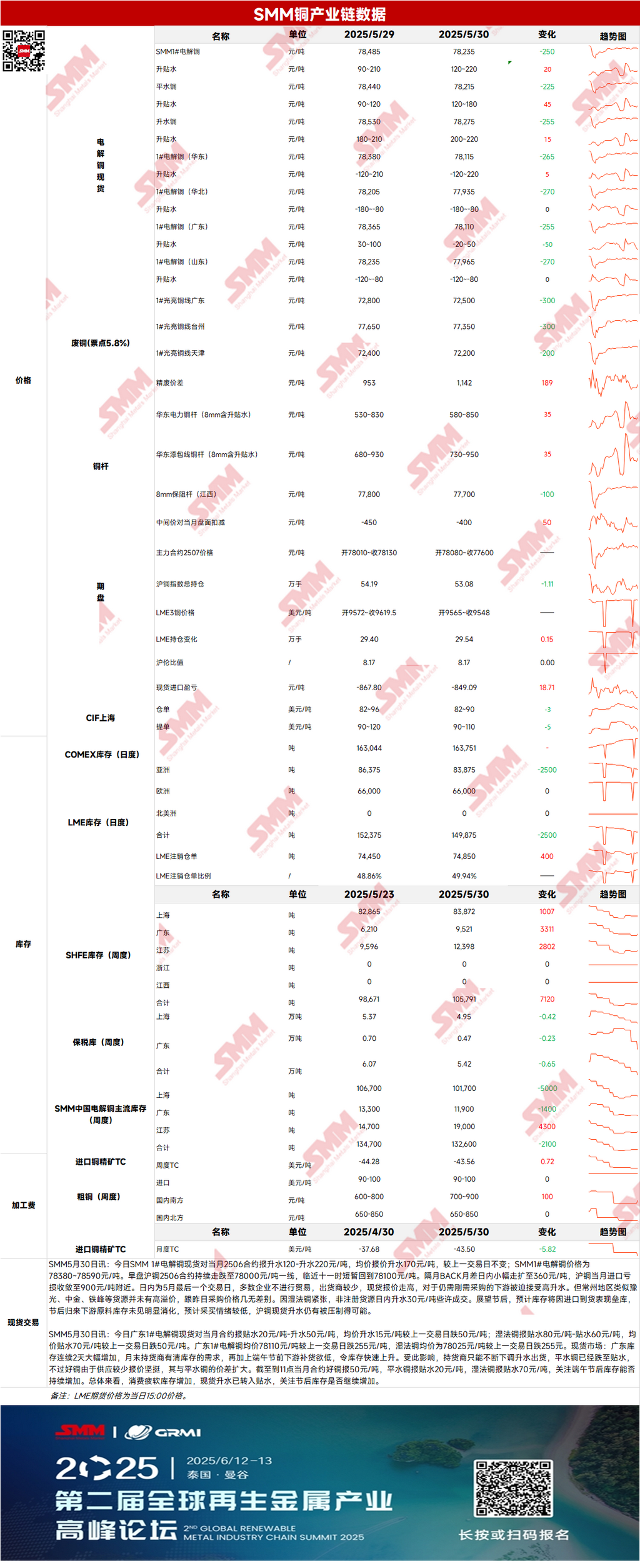

Spot: (1) Shanghai: On May 30, SMM #1 copper cathode spot prices against the front-month 2506 contract were quoted at a premium of 120-220 yuan/mt, with an average premium of 170 yuan/mt, unchanged from the previous trading day. The SMM #1 copper cathode price was 78,380-78,590 yuan/mt. In the morning session, the SHFE copper 2506 contract continued to decline to around 78,000 yuan/mt before briefly returning to 78,100 yuan/mt near 11 a.m. The BACK price spread between futures contracts widened slightly to 360 yuan/mt during the day, and the import loss for front-month SHFE copper narrowed to around 900 yuan/mt. Looking ahead after the holiday, inventory is expected to build up due to import arrivals. With no significant digestion of downstream raw material inventory expected after the holiday, purchasing sentiment is likely to remain low, and spot premiums for SHFE copper may still be suppressed.

(2) Guangdong: On May 30, Guangdong #1 copper cathode spot prices against the front-month contract were quoted at a discount of 20 yuan/mt to a premium of 50 yuan/mt, with an average premium of 15 yuan/mt, down 50 yuan/mt from the previous trading day. SX-EW copper was quoted at a discount of 80 yuan/mt to a discount of 60 yuan/mt, with an average discount of 70 yuan/mt, down 50 yuan/mt from the previous trading day. The average price of Guangdong #1 copper cathode was 78,110 yuan/mt, down 255 yuan/mt from the previous trading day, and the average price of SX-EW copper was 78,025 yuan/mt, down 255 yuan/mt from the previous trading day. Overall, weak consumption and rising inventory have led to spot premiums turning into discounts. Attention should be paid to whether inventory continues to increase after the holiday.

(3) Imported Copper: On May 30, warrant prices were $82-90/mt for QP June, with an average price down $3/mt from the previous trading day. B/L prices were $90-110/mt for QP June, with an average price down $5/mt from the previous trading day. EQ copper (CIF B/L) prices were $50-60/mt for QP June, with an average price down $12/mt from the previous trading day. Quotations were based on cargoes expected to arrive in early June. Overall, QP copper prices have fallen sharply, and the market expects buying activity to pick up after the holiday. If the SHFE/LME price ratio gradually improves, Yangshan copper premiums may find support at low levels.

(4) Secondary copper: On May 30, the price of secondary copper raw materials fell by 300 yuan/mt MoM. In Guangdong, the price of bare bright copper was 72,400-72,600 yuan/mt, down 300 yuan/mt from the previous trading day. The price difference between copper cathode and copper scrap was 1,142 yuan/mt, up 189 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 1,115 yuan/mt. According to an SMM survey, secondary copper raw material import traders indicated that COMEX copper prices pulled back this week, leading to a decrease in the absolute value of the minus for US secondary copper raw materials. However, LME copper prices only dropped slightly, so the discount coefficient quoted by local suppliers remained unchanged. In Europe, the local supply of secondary copper raw materials remained tight this week, so prices did not pull back.

(5) Inventory: On May 30, LME copper cathode inventories decreased by 2,500 mt to 149,875 mt. On the same day, SHFE warrant inventories increased by 1,963 mt to 34,128 mt.

Price: On the macro side, data showed that the US manufacturing sector contracted for the third consecutive month in May, putting pressure on the US dollar index, which hit a nearly six-week low, providing support for copper prices. Additionally, Trump indicated late last Friday that he plans to raise tariffs on imported steel and aluminum from 25% to 50% starting Wednesday, and hopes that countries will present their best offers for trade negotiations before Wednesday. Currently, US officials are attempting to accelerate negotiations with multiple trading partners before the end of the self-imposed five-week suspension period. Under the pressure of tariff threats, the US dollar is under pressure, providing support for copper prices. On the fundamental side, supply side, last Friday was the last trading day of May, with most enterprises halting trade and fewer shippers, leading to a temporary tightening of spot supply in the market and driving up spot quotes. Demand side, there is still some just-in-time procurement from downstream sectors, but they are forced to accept high premiums, resulting in relatively passive overall procurement behavior and no significant improvement in purchasing sentiment. Price-wise, copper prices are expected to remain supported today.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and not rely on this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]